.webp)

Home equity is a more common resource than government loans for small business ventures.

Amid high interest rates and a volatile business climate, small businesses may be struggling to secure the financing they need to launch or expand – especially micro-businesses, which typically have fewer than 10 employees and often fall between the cracks of government lending programs. Small entrepreneurs often rely on personal assets, such as their homes, to fund ventures when lending conditions are tight. Recently, there has been a surge in interest in small business startups in the District of Columbia and Virginia, possibly driven by career pivots among recently laid-off federal workers.

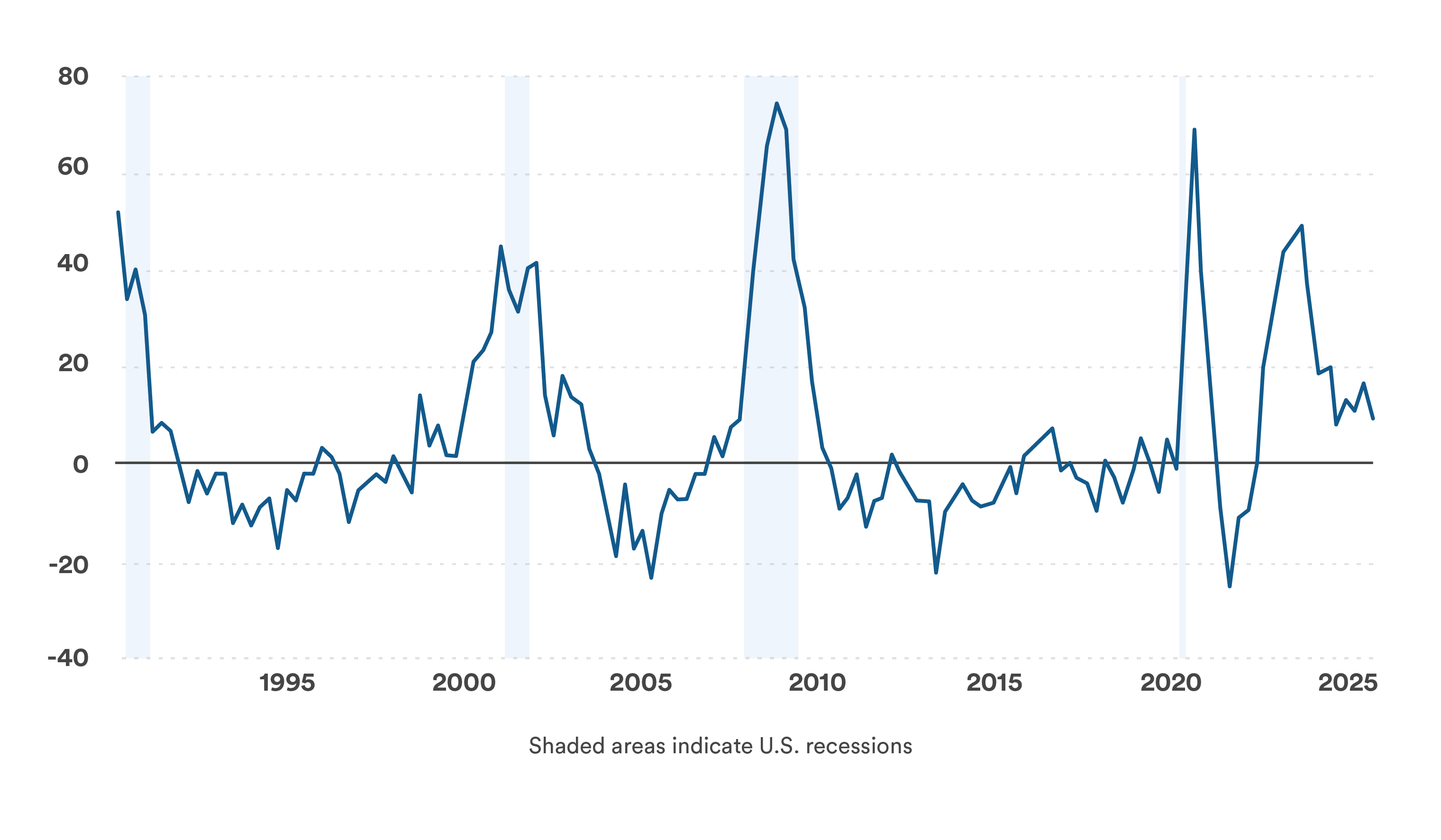

Lending standards for small businesses have tightened for 13 consecutive quarters, the longest string of bank tightening since the Great Recession

Lending conditions for small firms have tightened for 13 consecutive quarters through 2025-Q3, according to the Federal Reserve Board’s Senior Loan Officer’s Opinion Survey (SLOOS) – the longest period of tightening credit conditions since the end of the Great Recession in 20101. During previous stretches of tightening credit conditions, interest rates have declined sharply; that has not occurred (at least not yet) for the ongoing tightening cycle.

Net percentage of domestic banks tightening standards for commercial and industrial loans to small firms

Policy changes at the Small Business Administration are poised to continue adding headwinds to small business lending even as interest rates start to fall

Policy changes at the Small Business Administration (SBA) are poised to add additional pressure to small business lending, even as the Federal Reserve Board begins to ease lending conditions gradually. The changes are designed to limit taxpayer exposure to potential losses incurred by small businesses. Still, they will also have the net effect of making it more difficult for Americans seeking to buy, start, or expand a small business to access financing.

Personal assets are commonly used to start small businesses

According to the Census Bureau’s 2022 Annual Business Survey – the most recent data available – roughly 10% of small businesses use personal assets, another 10% use personal credit cards to launch their business, and one in 16 reports using home equity. Home equity is a more common source of financing than government loans for small business ventures. For micro-businesses, the share is likely even higher.

Funding sources for small businesses from the Census Bureau’s Annual Business Survey

(1) Family & friends, grants, VCs, & other sources;

(2) Federal, state and local government guaranteed loans.

Americans who want to start businesses appear to be using Home Equity Investments as an alternative to traditional sources of startup financing, like bank loans

The share of Home Equity Investment (HEI) inquiries to Point that cite small business investment as a use for the investment has doubled from 3.8% in 2019-Q1 to 7.0% in 2025-Q3. Small business investment has steadily trended higher over the past six years and is one of the fastest-growing use cases among Point customers. Homeowners are sitting on record levels of home equity. With no income underwriting or monthly payments required for an HEI — and higher interest rates on alternative products — an HEI is a natural source of funding for many small entrepreneurs.

Over the six years from 2019 to 2025 — a period that spans a full easing-and-tightening cycle for small business commercial and industrial lending conditions, according to SLOOS — interest in accessing home equity for small business investment was consistently higher during quarters when lending conditions were tightening. On average, 6.5% of Point HEI inquiries referenced small business investment when the SLOOS signaled easing small business lending conditions, compared to 7.4% when the SLOOS signaled tightening small business lending conditions.

Small business investment requests by lending condition

Average quarterly share of total requests

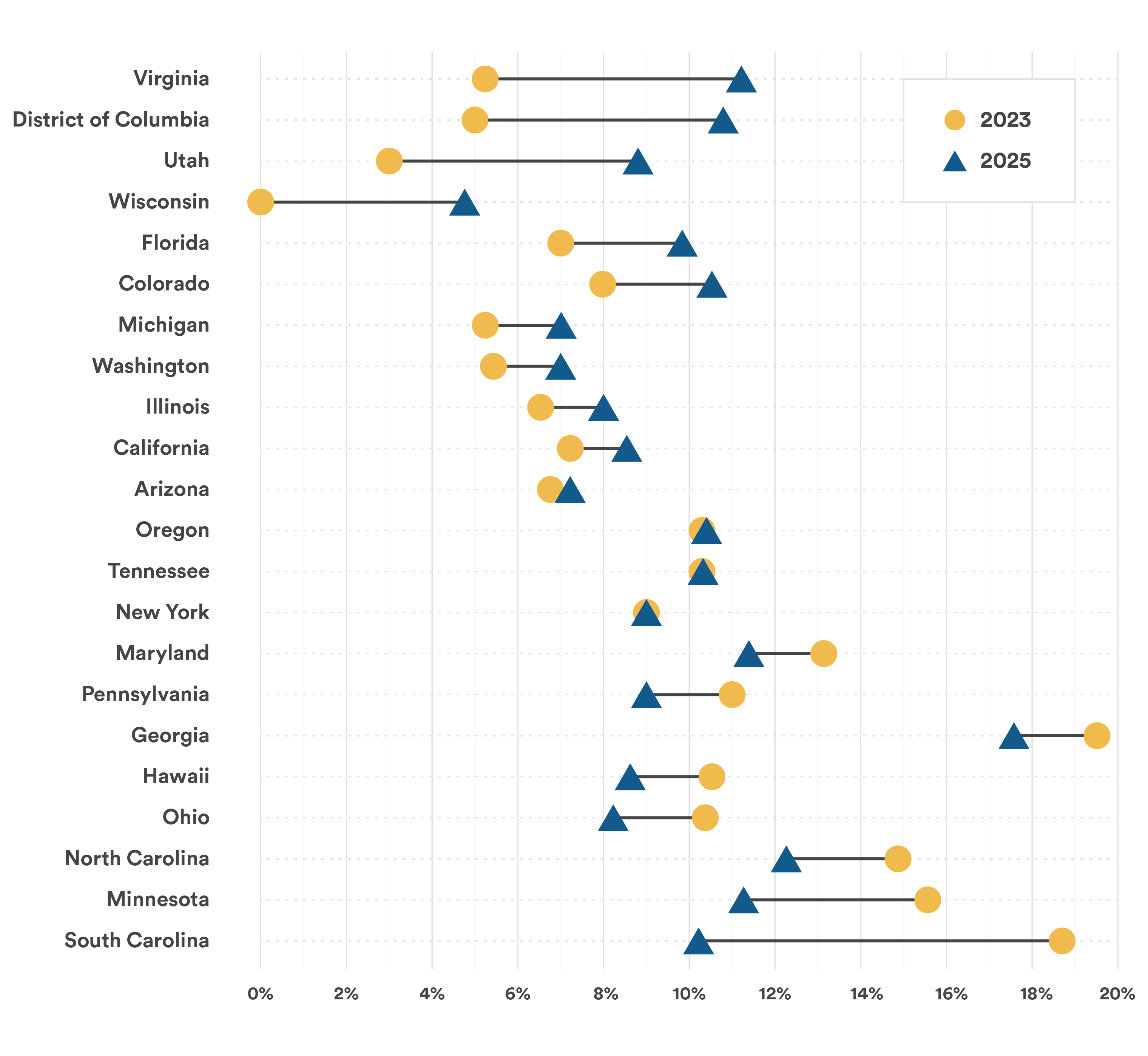

While large states account for most HEI inquiries for small business investment, there has been a surge recently in the District of Columbia and Virginia

Four large states – California (20.5%), Florida (17.1%), New York (7.2%), and North Carolina (5.8%) – account for half of all home equity investment inquiries intending to use the funds to start or expand a small business2. These states account for 28% of the U.S. population and 22% of new business starts. North Carolina appears to be punching above its weight.

The growth story is, perhaps, more interesting. The states that saw the largest increases in small business investment – as measured by the share of HEI inquiries in each state that are intended for small business investment – are Virginia (+6.2 percentage points from 5.3% of HEI inquiries in 2023 to 11.5% in 2025) and the District of Columbia (+4.8 percentage points from 5.0% to 10.8%) – likely driven by recently laid off federal government employees pivoting into entrepreneurial ventures.

Utah, Wisconsin, Florida, Colorado, Michigan, and Washington State also saw smaller increases in the share of HEI inquiries referencing small business investment, while South Carolina, Minnesota, and North Carolina saw the largest declines from 2023 to 2025.

Small business investment requests by lending condition

Micro-businesses often fall through the cracks of government small business lending programs

There does not appear to be a statistical relationship between Small Business Administration (SBA) lending activity and small business startup interest in Point HEI inquiries, suggesting that the two financing sources likely serve different audiences. The reality is that small business ventures – and especially microbusinesses – often fall between personal consumer lending and business lending. Founders often rely on personal savings or assets during the planning and launch phases. In the federal government’s fiscal year 2025, the average loan amount for the most extensive SBA lending program – the 7a program, which guarantees loans for a broad range of purposes like working capital, inventory, and equipment – was $470,267. By comparison, the average amount requested by Point HEI inquiries in 2025 for small business investment was $116,575, and 98.9% of inquiries were below the SBA 7 (a) average.

In general, there appears to be a “missing middle” in small business funding needs – funding that is larger than can be put on a personal credit card, but less than is typically available for formal bank or government-backed lending programs. HEI appears to often fill this funding niche.

Food service businesses are the most common type of small business venture funded with HEI funds, accounting for over a third of those who indicate a business investment

Not all HEI inquiries indicate the type of small business they plan to invest in, but among those that do, the top categories are:

- Food service – including food trucks, bakeries, coffee shops, bars, pizza parlors, and catering services: 37%.

- Construction – including general contractors, plumbing, electrical, HVAC, lawn care, and excavation: 28%.

- Professional services – including consulting, tech, and design: 13%.

- Transportation services – including trucking and taxi services: 10%.

- Hair and nail care – including salons, barbershops, and day spas: 7%.

Conclusion

Tight lending conditions for small businesses have been a headwind for micropreneurs, and recent changes to SBA lending guidelines are poised to tighten lending conditions further. Even in easier economic conditions, small businesses often rely on their founders' personal assets during the initial launch phase. Home equity fills a critical niche in funding small businesses that require more borrowing than can be put on a credit card, but less than is typical of formal business lending programs.

No income? No problem. Get a home equity solution that works for more people.

Prequalify in 60 seconds with no need for perfect credit.

Show me my offer

Frequently asked questions

Thank you for subscribing!

.webp)

You’re good to go — enjoy your resource.

You’re good to go — enjoy your resource.

Frequently Asked Questions

1 The SLOOS definition of small businesses includes firms with annual sales less than $50 million

2 Point does not operate in all 50 states.